Understanding the social security 5-year rule can be a daunting task.

This regulation, though complex, plays a pivotal role in how disability benefits are distributed and received.

The social security 5-year rule, if not fully grasped, can leave beneficiaries puzzled about their entitlements.

In fact, many individuals find themselves unprepared when they face sudden changes to their income or health status due to this rule’s implications.

Decoding the Social Security Disability Five-Year Rule

The five-year rule is a significant aspect of the Social Security Disability Insurance (SSDI) program, overseen by the Social Security Administration. This provision aids individuals who have previously received SSDI benefits and are once again unable to work due to recurring or aggravated disabilities.

This rule provides an exemption from standard waiting periods for such beneficiaries. To qualify under this guideline, one needs to accumulate sufficient work credits through social security covered employment over their lifetime. The current law allows earning up to four credits per year based on annual income.

Who Stands Benefited From The Five-Year Rule?

In general terms, anyone who has received SSDI benefits in the past can potentially benefit from this regulation if they face disability within five years after the termination of the previous claim. However, these individuals must still fulfill all other prerequisites set forth by the SSA, including proving that they are incapable of substantial gainful activity because of a medically determinable physical or mental impairment which lasts continuously for at least 12 months or results in death.

Besides directly related cases involving the recurrence of disability among former recipients, it’s worth noting here another variant – social security spouse’s benefits wherein surviving spouses might also be eligible provided certain criteria outlined by the SSA regarding age and relationship status are met, amongst others.

Decoding the Social Security Five-Year Rule

The Social Security five-year rule is an essential part of the Disability Insurance program, granting those who have had disability benefits in the past and then experienced another disabling incident within a period of five years to restart their advantages without going through the normal waiting time. It provides individuals who have previously received disability benefits and then suffered another disabling event within a span of five years an opportunity to restart their benefits without undergoing the usual waiting period.

To delve deeper into how work credits contribute towards qualifying these beneficiaries, resources from the Social Security Administration provide comprehensive information.

Navigating Exceptions to The Five-Year Rule

In terms of exceptions related to this general guideline about restarting SSDI payments under the five-year rule, there are certain specific circumstances worth considering. One such scenario pertains directly to Social Security spouse’s benefits.

- If someone was receiving spousal or survivor’s benefit based on their partner’s record and they become disabled themselves within seven years following their spouse’s death, they might be eligible for disability payments even if they haven’t worked recently enough as per standard rules.

- A transitional phase also exists where recipients can test out returning back into the workforce while still being able to receive full SSDI payments. This trial work period lasts nine months spread across any rolling 60-month window – consecutive months aren’t mandatory here.

- Earnings above annual limits set by the SSA during this phase won’t cause immediate cessation but will trigger an extended three-year period ending where monthly checks continue whenever total wages fall below the substantial gainful activity level defined by current law.

Impact of Reaching Full Retirement Age on SSDI Benefits

The SSDI program is a vital source of support for individuals unable to work due to disability. However, it’s crucial to understand the transformation these benefits undergo when recipients reach their full retirement age.

When you reach your full retirement age, your SSDI benefits seamlessly transition into Social Security retirement benefits. This change doesn’t require any action from beneficiaries and ensures that the amount received remains consistent since it’s based on lifetime earnings before disability onset rather than recent income changes or employment history.

This automatic conversion comes with several perks for those receiving these funds. Most notably, there are no longer restrictions on how much money can be earned through employment while still collecting these payouts. According to SSA guidelines, after reaching full retirement age, you will receive the total benefit regardless of additional income generated through labor.

No Matter Your Age: Hold Off Claiming Benefits Until You Reach this Milestone

In light of understanding how reaching full retirement age impacts Social Security Disability Insurance payments, one can see why financial experts often recommend delaying claiming early retirements whenever feasible. GoBankingRates suggests waiting until at least “full” retirement – if not later – as a strategy to maximize potential monthly payments in future years.

If an individual opts for early withdrawal options available between ages 62-65 depending on birth year, they’re likely facing permanent reductions in their monthly payout compared with what would have been awarded had they waited until achieving ‘full-retirement-age’. Therefore, patience indeed pays off when dealing with complex systems like Social Security by ensuring the maximum possible lifetime benefit amounts.

Decoding the Eligibility Criteria for SSDI Benefits

The SSDI program, a part of Social Security benefits, is intended to provide assistance to individuals who are medically unable to work. The eligibility requirements for this program involve two critical earnings tests – the recent work test and the duration-of-work test.

To qualify under the definition of disability, as outlined by the SSA, applicants must demonstrate an inability to perform any substantial gainful activity owing to their medical condition(s). This implies that these health issues should be either terminal or expected to last at least one year.

Navigating Through the Process: Applying for SSDI Benefits

Filing an application with the SSA can take place online or in-person via scheduled appointments at local offices. For those comfortable with technology and seeking convenience, applying online could be beneficial.

You can begin your journey on the Social Security Disability Application portal. Detailed instructions here guide you through each step accurately while ensuring all necessary information like personal details, employment history, and specifics about your medical conditions are provided properly.

If digital platforms aren’t accessible or preferred over traditional methods, there’s always the option of scheduling visits to nearby offices using the handy tool called the Social Security Office Locator.

Earnings Tests: Unraveling the Recent Work Test & Duration-of-Work Test

These two tests assess the applicant’s working history before the onset of disability. The ‘recent work’ test focuses on how recently they’ve worked, whereas the ‘duration-of-work’ test evaluates the total time spent employed during which Social Security taxes were deducted from income under the current law governing the Social Security system.

- Varying Requirements Based On Age:

Different age groups have different criteria set forth by these tests, making them increasingly stringent as one ages. For

Key Takeaway:

Understanding SSDI benefits eligibility hinges on two earnings tests – the recent work test and duration-of-work test. It’s crucial to prove inability to perform any substantial gainful activity due to medical conditions, which must be terminal or expected to last a year. Applications can be made online or in-person at local SSA offices.

Decoding the Social Security 5-Year Rule for Financial Pros

Explore the social security 5-year rule’s impact on disability benefits, retirement age, and Medicare. Unravel complexities with our guide.

Unraveling the Link Between Social Security Five-Year Rule and Medicare IRMAA

Navigating the complexities of retirement planning can be daunting for financial professionals, especially when it comes to understanding how different rules interact. A prime example is deciphering the connection between the social security five-year rule and Medicare’s Income-Related Monthly Adjustment Amount (IRMAA).

The crux of this relationship lies in income changes that may occur as a result of reentering employment after receiving disability benefits under the social security five-year rule. These new earnings could potentially escalate an individual into a higher bracket for calculating Medicare Part B and Part D premiums, leading to increased costs due to IRMAA.

Digging Deeper: How Changes Impact Your Client’s Premium Costs

To comprehend why these changes might affect your client’s premium amounts, you need to understand how IRMAA calculates adjustments based on modified adjusted gross income (MAGI). The key factor here is that MAGI calculations are determined by looking back two years at tax returns filed with the IRS via current law governing the social security system.

This means any significant fluctuations in your client’s income during those three years ending could alter their future premium payments – something they should definitely prepare for while reaching full retirement age.

Potential Scenarios That Could Lead To Higher Costs

If we consider potential scenarios, one situation involves clients who had no taxable earnings but then started earning again through employment or self-employment facilitated by SSDI benefits from the application of the social security five-year rule; such fresh earnings would impact MAGI calculation hence raising the monthly adjustment amount.

Key Takeaway:

Deciphering the Social Security 5-year rule’s impact on disability benefits, retirement age, and Medicare can be a tough nut to crack for financial pros. A key takeaway is that new earnings after reentering employment post-disability could potentially hike up an individual’s Medicare Part B and Part D premiums due to IRMAA calculations based on MAGI.

Preparing for Retirement Amidst Changing Life Spans

The increase in life spans has dramatically reshaped retirement planning. It’s now more important than ever to account for a longer period of income during your post-work years, including maximizing Social Security benefits and other lifetime benefits.

A common strategy financial professionals recommend is delaying the claim of Social Security until you reach full retirement age or beyond. This allows recipients to maximize their monthly benefit amount – an essential move considering extended life expectancies.

1. Diversify Your Income Sources

It is essential to contemplate other income sources, such as individual savings, investments, pensions and annuities, when planning for retirement aside from deciding when to claim Social Security. The SSA provides comprehensive information about potential changes, which could affect how much individuals receive upon reaching full retirement age under current law.

2. Stay Informed About Changes

Navigating these rules can be complex, but understanding them thoroughly will help make strategic decisions regarding claiming your benefits. Here are three ways to recession-proof your retirement regardless of future legislation or market trends.

4 Key Points To Remember When Planning For Retirement:

- Diversification: Create multiple streams of income that include not just Social Security but also personal savings and investments.

- Educate Yourself: Familiarize yourself with any changes in the laws related to the Social Security five-year rule work and understand its implications on SSDI Benefits conversion.

- Patiently Wait Until Full Retirement Age: If possible, delay claiming Social Security until you reach full retirement age to reap maximum rewards from this system.

Navigating the Social Security Disability System with Legal Assistance

The Social Security disability system, especially rules like the five-year rule and the current law governing it, can be complex. This complexity often necessitates seeking assistance from experienced Social Security disability attorneys.

These legal professionals have a deep understanding of the nuances involved in SSDI benefits conversion, eligibility criteria, and the potential impact on Medicare IRMAA. They are adept at guiding clients through all necessary steps while ensuring paperwork is correctly completed.

Advantages of Engaging an Attorney

Apart from their extensive knowledge about laws related to full retirement age or lifetime benefits under SSA, these lawyers also provide invaluable help during appeals if your initial application for SSDI gets denied by SSA. Research has shown that individuals who hired representation had significantly higher success rates than those without legal aid during hearings.

In addition to improving chances at appeal stages, they can assist you in gathering crucial medical evidence supporting your claim or even representing you before an administrative law judge when required.

Finding the Right Lawyer for Your Needs

Selecting a competent lawyer may seem overwhelming amidst dealing with health issues and financial stressors associated with reaching retirement age. However, there are resources available that make this process easier by providing comprehensive listings of experienced attorneys across various regions.

- You should look into factors such as their experience level within SSDI cases specifically,

- Their fee structure (many work on a contingency basis),

- Client reviews,

- and any potential disciplinary actions against them while choosing one.

This will ensure that they align well not only professionally but personally too, so as to best serve your unique requirements throughout the journey towards securing rightful benefits under the current law governing the Social Security Administration’s programs.

Key Takeaway:

Untangling the web of Social Security disability rules, like the five-year rule, often calls for a seasoned legal hand. A skilled attorney can guide you through SSDI benefits conversion and eligibility criteria while increasing your chances at appeal stages. Finding the right lawyer isn’t just about professional alignment; it’s also about personal fit to best serve your unique needs.

Conclusion – Maximizing Benefits Under Current Law

The complexities of the Social Security disability five-year rule can seem overwhelming, but with a thorough understanding, financial professionals are better equipped to guide their clients through this intricate system.

We have examined how reaching full retirement age influences when one should claim benefits. The No Matter Your Age, Do Not Claim Benefits Until You Reach This Milestone article provides further insights on this topic.

Navigating SSDI Eligibility Criteria

To qualify for SSDI benefits under current law governing the Social Security system, applicants must meet the SSA’s definition of disability and pass two earnings tests – the recent work test and the duration-of-work test. These requirements increase with age and play an essential role in determining eligibility status.

The Intersection Between the Social Security Five-Year Rule and Medicare IRMAA

A critical aspect that requires attention is how changes in income due to reentry into the workforce might affect Medicare premiums via IRMAA. It underscores why it’s crucial to keep track of earning status as individuals approach retirement age.

Lifetime Benefit Management Amidst Changing Lifespans

In light of increasing lifespans, planning strategies around managing lifetime benefits effectively during retirement years become even more significant. 5 Ways To Recession-Proof Your Retirement offers valuable advice on preparing for longer retirements than previous generations anticipated.

Social Security Disability System Legal Assistance Necessity

When dealing

Conclusion

Yet, it’s a crucial aspect of planning for disability benefits and retirement.

The intricacies of this rule can impact your SSDI eligibility and even Medicare premiums.

Understanding how work credits contribute to these benefits is key.

Navigating through exceptions to the five-year rule requires careful attention.

Your full retirement age plays a pivotal role in converting SSDI into retirement benefits.

The connection between changes in income and IRMAA under Medicare isn’t straightforward either.

Together, let’s empower clients with accurate calculations on their IRMAA costs as part of their comprehensive retirement plan.

Table of Contents:

- Decoding the Social Security Disability Five-Year Rule

- Decoding the Social Security Five-Year Rule

- Impact of Reaching Full Retirement Age on SSDI Benefits

- Decoding the Eligibility Criteria for SSDI Benefits

- Decoding the Social Security 5-Year Rule for Financial Pros

- Unraveling the Link Between Social Security Five-Year Rule and Medicare IRMAA

- Preparing for Retirement Amidst Changing Life Spans

- Navigating the Social Security Disability System with Legal Assistance

- Conclusion – Maximizing Benefits Under Current Law

- Conclusion

Streamlining the Medicare Surcharge Calculation Process.

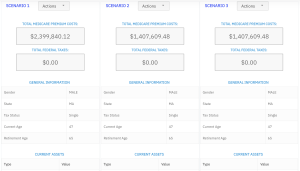

Our Healthcare Retirement Planner software is designed to streamline the retirement planning process for financial professionals. By providing an efficient way to calculate IRMAA costs, our tool helps you save time and focus on other aspects of your clients’ retirement plans.

- Faster calculations: Our software quickly calculates IRMAA costs based on your client’s income and tax filing status, eliminating manual calculations and potential errors.

- User-friendly interface: The intuitive design of our platform makes it easy for financial professionals to input data and generate results with minimal effort.

- Data integration: Seamlessly integrate our calculator into your existing financial planning tools or CRM systems for a more streamlined workflow.

- Easy to Understand Reports: Export reports to easily share with your clients

- Tax and Surcharge Modeling: see how different types of income affects both taxes and your surcharges.

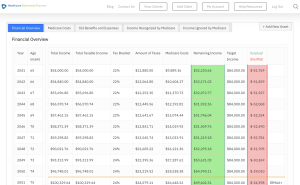

In addition to simplifying the calculation process, using our Healthcare Retirement Planner can also help improve communication between you and your clients. With clear visuals that illustrate how IRMAA costs impact their overall retirement plan, you can effectively convey complex information in an easily digestible format. This enables clients to make informed decisions about their healthcare expenses during retirement while ensuring they are prepared for any potential changes in Medicare premiums due to income fluctuations. To learn more about how our software can benefit both you as a financial professional and your clients’ retirement planning experience, visit the features page. Streamlining retirement planning processes can help financial professionals save time and resources, allowing them to focus on other areas of their clients’ needs. Automated calculation of IRMAA costs is the next step in streamlining this process even further.

- Ability to Run multiple comparison reports

- Easy to Understand Overview

- Quick IRMAA Indicator

- SimpleTax and Surcharge Display

- Detailed year by year reporting of income and expenses