When Does Medicare Start? Initial Enrollment

Our guide offers financial professionals key insights on when does Medicare start along with key dates.

Navigating Your Initial Enrollment Period

When Does Medicare Start? The initial enrollment period (IEP) for Medicare is a significant seven-month window that begins three months before your 65th birthday and concludes three months after. It’s during this time frame that the opportunity to sign up for Medicare presents itself.

Opting in within this period guarantees that seamless health care coverage begins without any penalties or gaps. However, missing out on enrolling during the IEP could mean waiting until the general enrollment period, which runs from January through March each year, with coverage starting only in July. An important note: late enrollees may face lifetime penalties impacting their Part B premiums.

Delaying Enrollment in Certain Circumstances

In some instances, delaying your Part B signup can be beneficial. Postponing enrollment in Part B of Medicare may be advantageous if you are employed and have health care coverage through an active employer or under a spouse’s job-based plan.

This delay can save unnecessary premium costs while having sufficient healthcare protection elsewhere. When such other insurance ceases or when one stops working (whichever happens first), an eight-month Special Enrollment Period kicks off, allowing individuals to enroll in Part B without penalty charges.

Remember, though: even if postponement seems viable now due to current job-related benefits, always keep track of changes like retirement dates so as not to miss out on timely opportunities.

Understanding the IEP and its implications is a critical component in ensuring a smooth transition into the Medicare system and avoiding future financial burdens.

When Does Your Medicare Coverage Begin?

The initiation of your Medicare medical insurance coverage hinges on when you enroll during the Initial Enrollment Period (IEP). This period kicks off three months before your 65th birthday and concludes three months after. It’s essential to comprehend how this timing impacts when your coverage starts.

Signing Up During or After Your Birthday Month

If you opt for Medicare Part A and/or Part B in the month of turning 65, or within the subsequent three-month span, there will be a delay in starting up your coverage. More specifically:

- In case enrollment happens concurrently with turning 65 – Expect commencement one month post-enrollment.

- A single month following hitting age 65 – Brace yourself for an additional two-month wait time.

- If it’s been two full calendar months since celebrating that milestone – You’re looking at a comprehensive waiting period spanning across another four weeks.

This implies that later IEP enrollment could result in several uninsured days or even longer stretches without coverages like hospitalization under Medicare Part A. Thus, early application is recommended whenever feasible. Social Security Administration (SSA), offers further details about these timelines as well as their implications regarding benefits start dates.

Bear in mind though; unique rules might apply if eligibility for Medicare arises due to disability. In most scenarios, however, individuals below the age threshold, i.e., younger than sixty-five years old suffering from certain disabilities, get automatically enrolled into Parts A & B commencing from the twenty-fifth consecutive disability benefit check either SSA or Railroad Retirement Board (RRB).

To ensure seamless healthcare transition devoid of gaps, financial professionals need to assist clients by incorporating such specifics into retirement planning calculations including IRMAA costs which are impacted by modified adjusted gross income (MAGI).

Key Takeaway:

Medicare medical insurance coverage start dates hinge on your Initial Enrollment Period timing, with potential delays if you sign up during or after your birthday month. Early enrollment is advised to avoid uninsured periods. Special rules may apply for disability eligibility, and financial professionals should factor these specifics into retirement planning.

How Other Insurance Impacts Your Medicare Enrollment

If you have other insurance, it’s crucial to understand how this can affect your decision on when to sign up for Medicare. Navigating the timing and coordination of benefits between Medicare and other insurance plans can be a complex task.

For instance, if you or your spouse are currently employed and covered by an employer-sponsored health plan, there may be options available that allow delaying enrollment in Part B of Medicare. This could potentially save money as long as the employer has more than 20 employees.

The Influence of Employer Coverage on Delaying Enrollment

Prioritizing existing health coverage through active employment over immediate Medicare Part B enrollment requires careful evaluation. Always consult with the human resources department or plan administrator first. They will provide guidance on whether their plan works well with Medicare, thus making delay beneficial both financially and healthcare-wise.

Note that COBRA and retiree health plans don’t count as employment-based coverage, so they won’t be eligible for a Special Enrollment Period once those coverages cease. Therefore, they don’t qualify for a Special Enrollment Period when those coverages end.

Navigating Multiple Insurances alongside Medicare

Holding multiple insurances including veterans’ benefits or TRICARE (for military retirees), each interacts differently with Medicare. For example, TRICARE generally necessitates beneficiaries enrolling into both Parts A and B while transitioning into the retirement phase from active duty service life.

In contrast, Veterans’ Affairs (VA) benefits operate separately from Medicare – Beneficiaries utilize either VA at VA facilities OR use Medicare at non-VA hospitals but not concurrently. Hence, understanding these nuances becomes essential before deciding about signing up for the initial enrollment period during the transition towards the retirement stage while holding such insurances.

The Impact of Medigap Policies

Medigap policies, supplemental private company sold policies aiding pay costs like co-payments, etc., which Original Medicare doesn’t cover, cannot be

Key Takeaway:

Key Takeaway: Navigating Medicare enrollment can be complex, especially when juggling other insurances. Understand the impact of employer coverage, COBRA, retiree health plans and Medigap policies on your decision to enroll in Medicare. Always consult with professionals for guidance before making a final call.

Common Misconceptions About When Coverage Starts

In the realm of Medicare coverage, there are several misconceptions that often lead to confusion and can result in costly errors. Let’s debunk some prevalent myths.

Misconception 1: Automatic Enrollment at Age 65

A common misunderstanding is believing that enrollment into Medicare automatically happens when one turns 65. In reality, unless you’re already receiving Social Security or Railroad Retirement Board benefits four months prior to turning 65, active enrollment during your initial enrollment period is required for Medicare coverage to begin.

Misconception 2: No Penalties for Late Enrollment

Another misconception suggests late enrollees face no penalties, which isn’t true. If not signed up during the seven-month window around their birthday month without having another qualifying health plan, late-enrollment penalties may apply. These additional charges could increase Part B premium by ten percent for each full twelve-month period where eligible but didn’t enroll.

Misconception 3: Post-65 Anytime Enrollment Without Consequences

The belief persists among many people that they can enroll anytime after age sixty-five with no consequences; however, this isn’t accurate outside certain special circumstances like qualifying Special Enrollment Period (SEP). Absent an IEP or SEP sign-up opportunity, beneficiaries must wait until General Enrollment Period from January through March every year with coverage starting on July first, potentially resulting in gaps in healthcare coverage.

All Parts of Medicare Start Simultaneously – Myth Debunked.

This final myth revolves around thinking all parts of Medicare start simultaneously. While Part A usually starts immediately upon enrolling, other parts such as Part D prescription drug plans or Medigap supplemental insurance policies might have different effective dates depending on when one signs up within respective open periods, making it important to double-check specific plan details before signing.

Key Takeaway:

Medicare enrollment isn’t automatic at 65 unless you’re receiving Social Security or Railroad Retirement Board benefits. Late sign-ups can incur penalties, and post-65 enrollments aren’t consequence-free outside special circumstances. Also, not all parts of Medicare start simultaneously; it’s crucial to check specific plan details.

Tips for a Smooth Transition into Your Medicare Coverage

Transitioning to Medicare can be a challenging process, yet with the correct help and comprehension of how it works, it’s achievable. This section provides tips on how to navigate this transition effectively.

Maximizing Benefits from Your Plan

The first step towards optimizing benefits is gaining an in-depth knowledge of what each Medicare Part A and B covers. For instance, while Part A primarily takes care of hospitalization costs, Part B includes doctors’ services along with outpatient care.

In addition to these basic parts, one might also consider additional plans such as Medigap or prescription drug coverage (Part D) that help cover expenses not included under original Medicare.

Avoidance of Late Enrollment Penalties

Late enrollment penalties are another aspect where being informed pays off. If you don’t sign up when you’re initially eligible during your initial enrollment period, premiums could rise due to late penalties. Therefore, timely enrollment before or after turning 65, unless specific circumstances allow delay without penalty, is recommended.

Moreover, keeping track of premium payment deadlines ensures there’s no delayed coverage starts or termination due to non-payment.

Navigating Through Different Enrollment Periods Effectively

The timing around when Medicare coverage begins depends heavily on enrolling within certain periods known as the Initial Enrollment Period (IEP), General Enrollment Period (GEP), etc. Knowing which period applies best according to one’s individual situation makes navigation easier.

The official medicarereseouces.org site offers detailed information regarding these different periods.

In conclusion, ensuring a smooth transition involves taking all relevant factors into account, including maximizing benefits by choosing suitable plan options, avoiding late fees through timely actions, and navigating effectively through various enrollment scenarios.

Table of Contents:

- Medicare Eligibility and Enrollment Basics

- When Does Medicare Start? A Guide for Professionals

- Navigating Your Initial Enrollment Period

- When Does Your Medicare Coverage Begin?

- How Other Insurance Impacts Your Medicare Enrollment

- Common Misconceptions About When Coverage Starts

- Tips for a Smooth Transition into Your Medicare Coverage

Streamlining the Medicare Surcharge Calculation Process.

Our Healthcare Retirement Planner software is designed to streamline the retirement planning process for financial professionals. By providing an efficient way to calculate IRMAA costs, our tool helps you save time and focus on other aspects of your clients’ retirement plans.

- Faster calculations: Our software quickly calculates IRMAA costs based on your client’s income and tax filing status, eliminating manual calculations and potential errors.

- User-friendly interface: The intuitive design of our platform makes it easy for financial professionals to input data and generate results with minimal effort.

- Data integration: Seamlessly integrate our calculator into your existing financial planning tools or CRM systems for a more streamlined workflow.

- Easy to Understand Reports: Export reports to easily share with your clients

- Tax and Surcharge Modeling: see how different types of income affects both taxes and your surcharges.

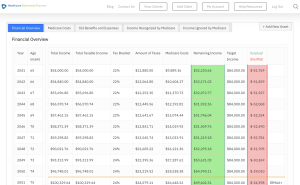

In addition to simplifying the calculation process, using our Healthcare Retirement Planner can also help improve communication between you and your clients. With clear visuals that illustrate how IRMAA costs impact their overall retirement plan, you can effectively convey complex information in an easily digestible format. This enables clients to make informed decisions about their healthcare expenses during retirement while ensuring they are prepared for any potential changes in Medicare premiums due to income fluctuations. To learn more about how our software can benefit both you as a financial professional and your clients’ retirement planning experience, visit the features page. Streamlining retirement planning processes can help financial professionals save time and resources, allowing them to focus on other areas of their clients’ needs. Automated calculation of IRMAA costs is the next step in streamlining this process even further.

- Ability to Run multiple comparison reports

- Easy to Understand Overview

- Quick IRMAA Indicator

- SimpleTax and Surcharge Display

- Detailed year by year reporting of income and expenses