Understanding the implications of SSA COLA 2024

is crucial for retirees.

This adjustment, made annually by the Social Security Administration (SSA), can significantly impact social security benefits and Medicare premiums.

The Social Security Cost-of-Living Adjustment (COLA) relies on data such as inflation, and traditionally changes with the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

Awareness about SSA COLA 2024, its calculation process, and potential effects empowers beneficiaries to plan their finances effectively.

The Dynamics of Social Security’s 2024 COLA

A surge in inflation caused a substantial jump in Social Security benefits, with an 8.7% COLA boost for beneficiaries by June 2023—a more significant annual rise than the previous 10 years.

This spike was indeed larger than the average annual increases observed over the past decade. However, experts forecast that we may see smaller COLAs for social security recipients come 2024 due to expected lower inflation rates and other economic factors taken into account by the Social Security Administration.

Potential Impact on Retired Workers’ Finances

Larger COLAs might seem advantageous at first glance as they lead to increased monthly payouts, but it is important not to look at these figures in isolation.

Inflationary trends can erode purchasing power faster than anticipated, which could offset any gains from higher benefit amounts. Therefore, understanding this dynamic is crucial when planning your retirement finances effectively.

Navigating Through Changing Economic Landscapes

To help navigate through such changing landscapes and understand how potential scenarios could unfold with regard to future adjustments in social security benefits, here’s a comprehensive guide you should consider reading. It provides detailed insights into various aspects, including understanding your benefit statement and predicting future payout amounts based on your current earnings record, among others.

How the Social Security Administration Calculates COLAs

The calculation of Cost-Of-Living Adjustments (COLAs) is a critical process performed by the Social Security Administration. The CPI-W, which gauges fluctuations in prices for goods and services consumed by urban dwellers, provides the data that shapes Social Security benefits. This index monitors average shifts over time in prices paid by urban consumers for goods and services. The data it provides directly influences social security benefits.

The Role of Inflation Data

Inflation holds significant sway when determining the Social Security COLA estimate. A rise in inflation typically leads to higher increases in COLA, while low or negative rates can result in smaller adjustments or none at all.

This relationship between social security benefits and inflation aims to preserve recipients’ purchasing power amidst economic fluctuations. For instance, if costs increase due to heightened inflation, so do social security payments through larger COLAs – this helps maintain beneficiaries’ financial stability.

To understand these trends better requires staying informed with up-to-date inflation data. By doing so, you as a financial professional are equipped with insights that allow you to anticipate potential adjustments accurately and strategize effectively around your clients’ retirement plans.

What a Smaller COLA Means for Retired Workers

A smaller COLA could have a considerable effect on retired workers, with even the tiniest adjustment potentially causing an alteration in their yearly benefit income. The most immediate effect is the potential alteration in monthly benefits, considering that even a minor percentage increase can translate into considerable extra income over an entire year.

Impact on Medicare Part B Premiums

Beyond directly influencing Social Security benefits, changes in COLAs indirectly affect Medicare Part B premiums. These are deducted from Social Security checks and typically rise each year due to inflation and healthcare costs.

If the growth of these premiums outpaces that of COLAs, retirees may see their net social security income decrease after paying Medicare expenses. This interconnectedness highlights how decisions or trends affecting one aspect often have ripple effects across others as well.

Taking into account the forecasted 3% COLA increase would add approximately $55.12 per month to an average retiree’s check – it becomes evident why financial professionals need tools like our Healthcare Retirement Planner when crafting comprehensive retirement strategies for clients who heavily rely on Social Security benefits.

The Silver Lining to Smaller COLAs

At first glance, smaller cost-of-living adjustments (COLAs) may seem like a drawback for Social Security recipients. However, when looking closer at these financial modifications, there’s more to it than initially thought. The true impact of these changes becomes evident when we consider inflation rates and their effect on buying power.

The Impact on Buying Power

If we take into account a situation where both the annual COLA increase and yearly inflation stand at 1%, beneficiaries would see only minor additions in benefits, but they wouldn’t lose ground as prices aren’t surging either.

Navigating High Inflation Periods

A different scenario emerges during periods of higher-than-normal inflation, despite unusually large COLAs being granted by the Social Security Administration. Retired workers might still find themselves grappling with increased costs that outpace their augmented income from Social Security benefits.

Beyond Numbers: Real-World Impacts

Rather than fixating solely on whether next year’s COLA will be larger or smaller compared to previous years’ increases, retirees should focus more on preserving buying power, according to various experts in this field.

This approach allows retirees not only to understand how much they’re going to receive in terms of dollars but also what those dollars can actually buy, which ultimately matters most.

Understanding the Implications of SSA COLA 2024 for Retirees

Discover how changes could affect social security benefits and Medicare premiums.

Staying Updated with Social Security Changes

Navigating the shifting landscape of social security requires an up-to-date knowledge base. Being informed about policy changes and adjustments is crucial for financial professionals, especially when it comes to retirement planning.

Latest Updates on Social Security’s COLA Estimate

The Social Security’s latest COLA estimates, as outlined in the annual report released by the Social Security Administration, can significantly impact beneficiaries’ financial strategies. Let’s break this down further:

- If 2024 sees smaller colas as predicted, retired workers may face a reduction in additional income.

- This isn’t necessarily all bad news though – lower inflation rates could mean that even with fewer dollars coming in from social security benefits, retirees might be able to afford more than before.

Besides these regular reports from the administration itself, there are other reliable sources such as credible news outlets and specialized websites providing timely information about any developments or changes related to social security policies. It’s essential we stay tuned into these platforms regularly.

In addition to general policy updates or modifications like those affecting calculations of COLAs or IRMAA costs, understanding specific aspects tied directly into different types of benefits also aids comprehensive retirement planning efforts.

.

- A deep dive into spous

Understanding the Implications of SSA COLA 2024 for Retirees

Discover how changes could affect social security benefits and Medicare premiums.

Conclusion

Inflation data and its role in determining COLAs have been discussed at length.

The potential implications of smaller COLA on Social Security benefits and Medicare Part B premiums can’t be overlooked.

However, it’s not all gloom with lower inflation rates potentially increasing buying power for beneficiaries.

Awareness about changes in Social Security policies and adjustments is key to financial planning.

If you’re looking to make sense of these complexities, Healthcare Retirement Planner is here to help! We specialize in assisting financial professionals calculate IRMAA costs as part of retirement plans.

We can guide you through the intricacies of SSA COLA 2024, helping ensure that your retirement plan accounts for any changes in Social Security benefits or Medicare premiums. Visit our site now to get the ball rolling!

Table of Contents:

- The Dynamics of Social Security’s 2024 COLA

- How the Social Security Administration Calculates COLAs

- What a Smaller COLA Means for Retired Workers

- The Silver Lining to Smaller COLAs

- Understanding the Implications of SSA COLA 2024 for Retirees

- Understanding the Implications of SSA COLA 2024 for Retirees

- Conclusion

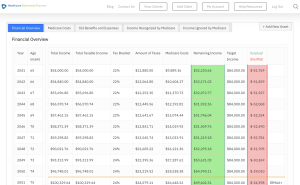

Streamlining the Medicare Surcharge Calculation Process.

Our Healthcare Retirement Planner software is designed to streamline the retirement planning process for financial professionals. By providing an efficient way to calculate IRMAA costs, our tool helps you save time and focus on other aspects of your clients’ retirement plans.

- Faster calculations: Our software quickly calculates IRMAA costs based on your client’s income and tax filing status, eliminating manual calculations and potential errors.

- User-friendly interface: The intuitive design of our platform makes it easy for financial professionals to input data and generate results with minimal effort.

- Data integration: Seamlessly integrate our calculator into your existing financial planning tools or CRM systems for a more streamlined workflow.

- Easy to Understand Reports: Export reports to easily share with your clients

- Tax and Surcharge Modeling: see how different types of income affects both taxes and your surcharges.

In addition to simplifying the calculation process, using our Healthcare Retirement Planner can also help improve communication between you and your clients. With clear visuals that illustrate how IRMAA costs impact their overall retirement plan, you can effectively convey complex information in an easily digestible format. This enables clients to make informed decisions about their healthcare expenses during retirement while ensuring they are prepared for any potential changes in Medicare premiums due to income fluctuations. To learn more about how our software can benefit both you as a financial professional and your clients’ retirement planning experience, visit the features page. Streamlining retirement planning processes can help financial professionals save time and resources, allowing them to focus on other areas of their clients’ needs. Automated calculation of IRMAA costs is the next step in streamlining this process even further.

- Ability to Run multiple comparison reports

- Easy to Understand Overview

- Quick IRMAA Indicator

- SimpleTax and Surcharge Display

- Detailed year by year reporting of income and expenses